Situation prior to the crisis

The American International Group (AIG) is a multinational finance and insurance corporation with operations in more than 80 countries. The company provides a wide range of services including general insurance, life insurance, retirement services, and financial services.

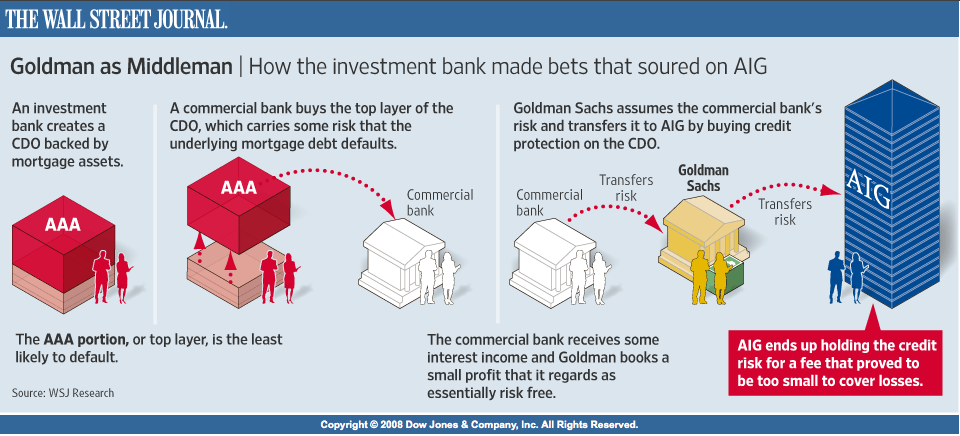

Before the 2008 financial crisis, AIG, a multinational finance and insurance corporation, was globally recognized. A division, AIG Financial Products (AIGFP), began dealing with complex derivatives called Credit Default Swaps (CDS), insurance contracts on financial instruments, notably mortgage-backed securities. During the U.S. housing boom, AIGFP wrote CDS contracts on these securities, assuming the risk of wide-scale mortgage default was minimal.

By 2007, AIG's exposure to these securities was immense due to the CDS contracts, obligating them to cover losses upon default. However, when the housing market slowed and mortgage defaults surged, the value of the securities dropped, leading AIG to face potentially catastrophic losses.

AIG's pre-crisis risk management systems faced criticism for not accurately accounting for a nationwide decline in home prices, and its corporate governance was deemed lacking. With over-reliance on positive credit ratings and inadequate risk management, AIG became exceptionally vulnerable to the housing market downturn.

Overall, the situation prior to the crisis was characterized by high-risk, high-reward strategies adopted by AIG's Financial Products division, an over-reliance on positive credit ratings, inadequate risk management practices, and a lack of effective corporate oversight. This made AIG incredibly vulnerable to the housing market's downturn, setting the stage for the company's near-collapse during the 2008 financial crisis.

What went wrong

The collapse of AIG in 2008 resulted from various factors including inadequate risk management, faulty corporate oversight, flawed models, and broader systemic issues.

AIG failed to properly measure, monitor, and control the risks associated with their CDS and securities lending operations. They severely underestimated the risks tied to the CDOs they insured and didn't maintain sufficient capital or liquidity buffers, leading to a capital crisis during the financial meltdown.

Moreover, AIG's governance structures failed to adequately monitor the risks Moreover, AIG's governance structures failed to adequately monitor the risks

AIG's risk assessment models were based on flawed assumptions about the CDOs they insured and the behavior of the housing market. These wrong assumptions revealed the company's severe exposure when the subprime crisis hit.

Finally, AIG's distress caused significant contagion effects throughout the financial sector due to their role as a major counterparty and insurer, amplifying the crisis. The lack of transparency about AIG's exposure increased market panic, creating a vicious cycle of asset sell-offs, liquidity crunches, and bailouts.

In essence, AIG's near-collapse during the crisis can be attributed to poor internal risk management, inadequate oversight, flawed assumptions, and systemic issues in the broader financial sector.

Four questions related to the risk management process

What caused the crisis?

The AIG's crisis was a result of failing to properly understand or manage the risks involved with their aggressive expansion into the derivatives market, particularly credit default swaps (CDSs). When the U.S. housing market crashed, it significantly devalued the mortgage-backed securities (MBSs) insured via AIG's CDSs, revealing the company's high-risk exposure.

Moreover, AIG's risk assessment mechanisms were insufficient, leading to an underestimation of the risks associated with their CDS and securities lending activities. This was due to their heavy reliance on flawed models and assumptions that didn't adequately consider a nationwide housing market decline or the correlation risks within their insured CDOs.

On the control front, AIG lacked robust strategies for managing exposure to the CDS and securities lending markets. They also suffered from poor corporate governance and internal controls, exacerbating the situation.

The crisis was further intensified by a lack of transparency about AIG's risk exposures and weak regulatory oversight, hindering their ability to respond effectively. Lastly, AIG's deep interconnectedness with other financial institutions resulted in a contagion effect, amplifying losses and uncertainty in the wider financial system.

In summary, AIG's crisis resulted from a series of risk management failures, aggressive expansion into risky markets, lack of oversight, flawed risk models, and a systemic contagion effect that amplified the crisis beyond AIG.

What bet was being taken?

AIG made risky bets based on optimistic assumptions about the housing market and its financial instruments, particularly Credit Default Swaps (CDSs) and Collateralized Debt Obligations (CDOs). They assumed continuous housing market growth and low mortgage default rates, betting on the diversification and low default correlations of their insured CDOs. They also presumed their CDS contracts wouldn't require collateral postings, and they'd have continuous access to affordable funding. When the housing market crashed, these assumptions failed, leading to AIG's severe financial losses, revealing major flaws in their risk management process..

What risks were not known or not appropriately measured?

AIG's downfall during the 2008 financial crisis was precipitated by several misjudged or overlooked risks. These include a failure to anticipate the severe housing market downturn that led to a surge in defaults on insured Mortgage-Backed Securities (MBSs). AIG did not foresee the necessity for large collateral postings, resulting in a liquidity crisis. The company's risk models leaned heavily on overly optimistic credit ratings. They also underestimated the risks associated with their substantial exposure to the single sector, the housing market. AIG miscalculated the credit quality, valuation, and correlation risks of the Collateralized Debt Obligations (CDOs) they insured. The company failed to properly measure risks tied to their securities lending activities and potential credit rating downgrades. Moreover, AIG overlooked systemic risks arising from their deep interconnectedness with other financial institutions. Finally, a lack of transparency about the company's exposure fed into market panic and distrust. In summary, AIG's collapse was driven by multiple failures in risk recognition and measurement.

What were the lessons learned?

There were several key lessons from AIG's near collapse. A primary takeaway is the importance of robust risk management. Companies need strong frameworks to accurately assess and manage risks, which includes conducting stress-tests and scenario analysis to anticipate losses during market downturns.

Another lesson is the need to fully comprehend complex financial products. Institutions dealing with intricate instruments like CDSs must grasp the underlying assets, potential loss scenarios, and the potential scale of these losses.

Regulatory oversight is also a crucial learning point. Regulatory bodies must possess the required expertise, resources, and authority for effective supervision of large, complex financial institutions. This involves understanding the risks linked to these institutions' activities and taking necessary measures to mitigate such risks.

Effective corporate governance is another key lesson. An independent board of directors can ensure oversight of a company's activities, comprehending the associated risks and ensuring that these risks are managed properly.

Transparency also emerged as a critical requirement. Financial institutions must clearly articulate their activities and associated risks to stakeholders and regulators. This involves offering understandable information about risk exposures and risk management practices.

In sum, the AIG case underscores the hazards of excessive risk-taking, opacity, and inadequate regulatory oversight in the financial industry, offering vital lessons for all stakeholders.

Risk categories applied in the AIG context

Market Risk

Market risk refers to the potential for financial losses resulting from unfavorable changes in market prices and rates. This risk can stem from factors like interest rates, exchange rates, equity prices, or commodity prices. These fluctuations can significantly impact the value of financial investments and contracts, leading to potential losses.

In the context of AIG, market risk manifested in several forms. The company held a substantial portfolio of Credit Default Swaps (CDSs), which were heavily tied to the performance of the U.S. housing market. AIG was essentially betting on the continued growth and stability of this market, but when the housing market unexpectedly collapsed, the value of the Mortgage-Backed Securities (MBSs) AIG insured took a significant hit. This situation led to large-scale defaults, causing AIG to suffer enormous losses as they had to fulfill the obligations of their CDS contracts.

Moreover, AIG also encountered market risk through its securities lending activities. It invested the cash collateral from lending securities into longer-term, less liquid assets such as MBSs. However, when the subprime mortgage crisis hit and the value of these assets decreased, AIG had to mark them to market, recognizing significant losses.

Lastly, AIG's CDS contracts required them to mark them to market based on the credit spreads of the underlying Collateralized Debt Obligations (CDOs). As the quality of these CDOs deteriorated during the financial crisis, these spreads widened. This change led to AIG having to recognize further losses and post additional collateral to its counterparties.

In essence, market risk, arising from its CDS portfolio and securities lending activities, played a crucial role in AIG's financial crisis. These situations exemplify how market risk can dramatically affect a company's financial standing, underlining the importance of robust risk management practices..

Counterparty Credit Risk

Counterparty credit risk refers to the risk that a counterparty in a financial contract will default or fail to meet its contractual obligations. It's a significant consideration for any financial institution engaged in transactions such as loans, derivatives, or repurchase agreements. This risk emerges from the potential default of a borrower, lender, buyer, seller, or a guarantor involved in these transactions.

For AIG, counterparty credit risk was present predominantly in its credit default swap (CDS) contracts and securities lending activities. The company wrote CDS contracts for various financial institutions, where it promised to pay these counterparties in case of default or credit events on the underlying collateralized debt obligations (CDOs). When the subprime mortgage crisis occurred and default rates on these CDOs spiked, AIG had to pay out on its CDS contracts, leading to significant financial losses.

In the context of its securities lending activities, AIG had to return securities or cash collateral to its counterparties upon their request. When these counterparties defaulted or withdrew their securities or cash collateral due to the financial crisis, AIG had to liquidate its assets at low, fire-sale prices or borrow funds at high costs to meet its obligations. These actions further deteriorated AIG's financial position.

Interestingly, in AIG's case, the counterparty credit risk turned out to be a secondary concern. The main risk was that AIG itself was at risk of defaulting on its obligations due to the falling value of the insured mortgage-backed securities (MBSs) and the impacts of the broader financial crisis. Nevertheless, the presence of counterparty credit risk in AIG's business model underscores the need for financial institutions to manage this risk effectively..

Liquidity Risk

Liquidity risk pertains to the danger that a firm may not be able to meet its short-term financial obligations due to its inability to convert assets into cash quickly and without significant loss. This risk can escalate during periods of financial turmoil, causing a significant drain on the firm's cash resources, and it becomes increasingly challenging to liquidate assets without substantial value loss.

In the context of AIG, the company faced acute liquidity risk during the 2008 financial crisis, primarily because of its credit default swap (CDS) contracts and securities lending activities. AIG's CDS contracts required the company to post collateral to its counterparties based on the mark-to-market value of the contracts and specific credit rating triggers. When the underlying collateralized debt obligations (CDOs) declined in value and AIG's credit rating was downgraded amid the subprime mortgage crisis, AIG had to post more collateral to its counterparties, significantly depleting its cash resources.

AIG's securities lending activities posed additional liquidity risk. The company had to return securities or cash collateral to its counterparties upon demand. During the crisis, as counterparties began to withdraw their securities and cash collateral, AIG was forced to liquidate its assets at fire-sale prices or borrow funds at steep costs to fulfill its obligations.

When the housing market collapsed, and the value of mortgage-backed securities (MBSs) fell sharply, AIG faced enormous collateral calls from its CDS counterparties. Despite holding substantial assets, AIG struggled to liquidate them quickly without incurring heavy losses. This scenario resulted in a severe liquidity crunch, eventually leading to the need for a government bailout.

Model Risk

Model risk refers to the potential for financial losses stemming from the use of financial models that rely on incorrect assumptions or fail to accurately capture the intricacies of financial markets. These models are often used for risk management, pricing, valuation, and measurement. Incorrect assumptions or oversights can lead to severe miscalculations, underestimating risk exposures, and subsequently, unforeseen losses.

American International Group (AIG) confronted substantial model risk, mainly through its credit default swap (CDS) contracts. AIG used models that made assumptions which turned out to be disastrously unrealistic in the wake of the subprime mortgage crisis. The company presumed that the collateralized debt obligations (CDOs) it insured were highly diversified and had low default correlations. It also assumed that a nationwide decline in the housing market was unlikely and that its CDS contracts would not necessitate collateral postings. Furthermore, the models operated on the assumption that AIG would always have access to cheap and abundant funding.

When the subprime crisis erupted, it brought about a steep decline in the value and liquidity of the CDOs, a surge in defaults and foreclosures, a collapse in AIG's credit rating, and a freeze in the credit markets. These drastic changes in market conditions starkly contradicted AIG's initial assumptions. In particular, the company had not considered a significant nationwide drop in housing prices, nor had it planned for the possibility of high default correlations between different mortgage-backed securities.

These model failures led to higher losses than expected when the housing market collapsed, highlighting the significant model risk AIG had taken on. AIG's experience underscores the importance of using robust, well-tested financial models that account for various market scenarios, and the potential disastrous outcomes if model risk is not properly managed.

Operational Risk

Operational risk refers to the potential loss due to inadequate or failed internal systems, processes, personnel, or from unforeseen external events. In the case of AIG, this type of risk manifested significantly.

Internally, there were substantial issues with AIG's risk management processes, which failed to identify or adequately manage the vast risks the company was undertaking through its involvement in the credit default swap (CDS) business. The governance structures within the company, intended to provide oversight and control, were also found wanting. AIG's Financial Products division, responsible for a large proportion of the risky CDS transactions, operated largely autonomously, with minimal effective oversight from the parent company. This lack of internal control allowed for the unchecked accumulation of risk that would eventually lead to the company's near collapse.

Exacerbating this internal vulnerability were a number of external factors. AIG was operating in a regulatory environment that failed to provide adequate supervision, a situation that further amplified the operational risk the company was exposed to. Moreover, the collapse of the housing market, and the associated crash in the value of mortgage-backed securities, which AIG had heavily insured, introduced an external shock that severely tested AIG's operational resilience.

Another contributing factor to AIG's operational risk was its compensation system, which had been designed to incentivize short-term profits. This design created an alignment of interest that encouraged risk-taking without adequately considering the potential for long-term consequences.

In conclusion, AIG's experience serves as a stark example of how internal and external factors can interact to escalate operational risk, ultimately pushing the company to the brink of failure..

References

- Kellogg School of Management. (2009). What Went Wrong at AIG? Kellogg Insight.

- Smith, R. (2019). Falling Giant: A Case Study of AIG. Investopedia.

- Lo, A. (2015). What We’ve Learned from the Financial Crisis. Harvard Business Review.

- Bluhm, C., Overbeck, L., & Wagner, C. (2013). Introduction to Credit Risk Modeling, Second Edition. CRC Press.

- McKinsey & Company. (2012). Getting to grips with counterparty risk. McKinsey Working Papers on Risk.

- Stanford University. (n.d.). Market Risk Management. Stanford Graduate School of Business.